By James Kwantes

Published first at Patreon

With apologies to Timothy Leary, summer is the time when many investors “turn on” (the music), “tune in” (to vacation vibes), and “drop out” (of the markets).

For others, money never sleeps. Some recent insider buys – including from resource “whales” known for creating shareholder value – captured my attention.

Lundin Mining (LUN-T)

The Lundin family’s third generation made quite a statement on July 29 by partnering with BHP, the world’s largest mining company, to purchase Filo and its exceptional Filo del Sol copper porphyry complex. BHP and Lundin Mining bought Filo for $4.5 billion, teaming up on a 50-50 basis in a deal that included Lundin Mining’s nearby Josemaria deposit.

Lundins 3.0: Well-fed and Hungry

Three days later, on August 1, Jack and Adam Lundin each spent about a million dollars adding to their personal stakes in Lundin Mining. Company chairman Adam Lundin, Lukas’s second son, purchased 75,000 at $13.23, taking his personal stake to 714,250 shares. Jack – the company’s president/CEO and Lukas’s third son – bought 74,000 shares at $13.24, giving him 430,556 shares. The share price has since sagged below the $13 level, following copper down on recession fears.

Lundin family trusts Zebra and Nemesia own a combined 119.4 million shares or 15.4% of shares outstanding, according to SEDI filings. The Lundins’ move to bring in a deep-pocketed partner on their impressive discoveries in the Vicuña district derisks development and helps secure the family legacy as world-class operators.

Price: $12.8

Shares out: 776.8 million

Market cap: $10 billion

Mirasol Resources (MRZ-V, MRZLF-OTC)

Mirasol is one of the less-promotional juniors active in the Vicuña district, where area plays have been sprouting up like forest mushrooms in a west coast winter. Mirasol is a project generator but its Sobek projects in Chile are 100% owned. Sobek North is 3 km west of NGEx Minerals’ (NGEX-V) high-grade Lunahuasi discovery; Sobek Central is 7 km west of Filo del Sol (investors going on site visits to Filo del Sol travel through Mirasol's Sobek property).

Mirasol has added to its land position through option deals with SQM and identified two promising zones with similar geological features to Filo del Sol (at Sobek Central) and to Lunahuasi (at Sobek North). Initial results have been positive but Mirasol’s programs have been hampered by everything from out-of-season snowfalls to washouts of access roads. Drilling is planned for Q4.

I featured Mirasol 10% holder Glenn Pountney in some of my first Patreon articles nearly two years ago. He’s still adding. On July 16, the veteran junior mining investor spent $60,000 to buy another 150,000 Mirasol shares at 40 cents. He purchased another $16,000 worth on August 6 following the big Filo news, also at 40 cents. Pountney now owns 8.515 million Mirasol shares, or 12.2% of the stock. Haywood’s John Tognetti owns 13.46 million MRZ shares, almost 19.3%.

Pountney was head equity trader at First Marathon Securities in the 1990s and has been racking up wins as a private investor ever since. He went above 10% shareholdings on the original Norsemont Mining and on Klondex Mines, both of which were acquired by majors.

Price: 0.41

Shares out: 69.8 million (71.8M fully diluted)

Market cap: $28.6 million

Augusta Gold (G-T, AUGG-OTC)

Richard Warke takes large stakes in companies within his stable, and it tends to work out well. His Ventana Gold, Augusta Resource Corp. and Arizona Mining sold for a combined $4.3 billion; he owned large positions in each. Augusta Gold’s stock symbol is G; Warke is an OG.

He has resumed buying shares of the developer, which has two wholly owned projects in Nevada’s Beatty district – home to the world-class Silicon-Merlin gold discoveries being developed by AngloGold Ashanti. The amounts aren’t huge, especially for a billionaire, but his ownership stake is. Warke, Augusta’s executive chairman, spent $16,000 in July purchasing shares at an average of 80 cents and another $3,500 on Aug. 9, at 69.5c. Warke owns 25.41 million Augusta shares, about 29.6% of the stock.

Augusta has been laying low – most of the news releases in the past year relate to loans and loan extensions from Augusta Investments, a private Warke company. But the mining tycoon is undoubtedly keeping a close eye on the rapidly growing gold district unfolding all around Augusta’s Bullfrog and Reward projects.

AngloGold Ashanti has 16.6 million gold ounces in Nevada, including a combined 13M oz (Indicated and Inferred) at the rapidly growing Silicon-Merlin deposits. Recent highlight drill intercepts at Merlin have included 144.5m of 10.53 g/t gold, 161.6m of 5.85 g/t and 190.4m of 5.12 g/t (all oxide hits).

Price: 0.79

Shares out: 86 million

Market cap: $67.9 million

Aurion Resources (AU-V, AIRRF-OTC)

Aurion has a dominant land position in an emerging gold district in Finland: the Central Lapland Greenstone Belt. The company’s portfolio includes joint ventures with B2Gold (BTO-T) and Kinross (K-T) as well as 100% owned ground where they have made gold and base metals discoveries. The most interesting project is probably Helmi, a gold discovery made just south and west of Rupert Resources’ 4M-oz Ikkari deposit. Aurion has 30% of Helmi in a JV with 70% owner B2Gold.

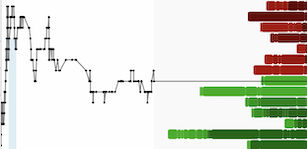

Rupert (RUP-T) has reason to be interested in the Aurion-B2Gold JV ground next door beyond just the gold. The outline of the Ikkari pit shell runs right to the JV property boundary (in red below), to the point where the border affects the shape of the proposed Ikkari pit and project economics. Back in March, Rupert offered B2Gold $102.8 million in RUP shares for its 70% share of the JV but the deal didn’t close; the standoff continues.

Ikkari is too good of a discovery – Rupert hit 4M oz through just 36,000 metres of drilling – to settle for a sub-optimal open pit, which would also be a sticking point for any Rupert acquirer. I expect a deal beneficial to Aurion shareholders.

Dave Lotan, Aurion’s chairman and second-largest shareholder, has much to gain from any transaction. He’s been adding to his stake through both public-market buys and in financings. He topped up in Aurion’s recent $9M financing (55c shares) by putting in $500,500 for another 910,000 shares. That took his balance to 14.817 million shares, or 9.95% of all shares – just behind Kinross, which participated in the financing to stay at 9.98%. Prior to the financing, Lotan had spent $220,370 buying shares since the beginning of July, at prices up to 63 cents.

Price: 0.55

Shares out: 148.9 million (159.4M fully diluted)

Market cap: $81.9 million

Galway Metals (GWM-V, GAYMF-OTC)

Galway Metals is drilling its Clarence Stream gold project in New Brunswick, which hosts an open-pittable resource of about 1.6M oz at 2 g/t gold with further ounces underground at grades above 4 g/t. Two rigs are turning and recent results including 19.5 g/t gold over 4.2 metres.

Galway CEO Robert Hinchcliffe has been a prolific buyer of the stock. Since the beginning of June, he has spent more than $220,000 purchasing Galway shares at prices ranging from 33.5 up to 54 cents. Last year Hinchcliffe bought 1.664 million Galway shares, according to a (rather curious) company news release on Aug. 13. He owns about 8.7% of outstanding shares.

Hinchcliffe founded Galway Resources, which sold for $340 million. Galway Metals is one of two spinoff companies and there have been some rollbacks along the way, allowing GWM to stay under 100M shares outstanding. Hinchcliffe’s pre-Galway career makes him worth watching – the former mining analyst was CFO of Kirkland Lake Gold (the original Kirkland Lake), which merged with Newmarket Gold and was ultimately sold to Agnico Eagle for $11 billion.

Galway has also bought back a 2% NSR royalty on claims within the Clarence Stream gold project. Such royalty cleanups can be a precursor to a sale. The stock has been on a bit of a tear since mid-July.

Price: 0.59

Shares out: 84.68 million (95M fully diluted)

Market cap: $50 million

Orogen Royalties (OGN-V, OGNRF-OTC)

I wrote about Orogen Royalties in Portfolio Cleanup Time in the Discount Aisle back in October 2022 with the stock at 42 cents and have touched on it a few times since. Based on a recent purchase, insider André Gaumond seems to think there remains upside from the current $1.41 level.

Orogen has a valuable 1% NSR on AngloGold Ashanti’s world-class Silicon-Merlin gold camp in Nevada and a cash-flowing 2% royalty on First Majestic’s Ermitano deposit in Sonora, Mexico. Orogen describes Ermitano as its flagship asset, but with Silicon-Merlin at 13 million ounces of oxide gold and counting, that will undoubtedly change.

World-class, Under the Radar Gold. How to Play It

Gaumond was a previous buyer of Orogen shares at 40 cents and in the high .50s, so a recent small purchase at $1.40 caught my attention. On Aug. 15 Gaumond bought $1,540 worth of shares. Gaumond is an insider of Orogen as a director of Altius Minerals (ALS-T), which owns about 18.1% of Orogen shares as well as 1.5% royalty on Silicon-Merlin.

Gaumond founded Virginia Gold Mines and spinout Virginia Mines, which sold for almost $1 billion combined. Read more about Gaumond here:

Follow the Leaders (Andre Gaumond edition)

Price: $1.41

Shares out: 201.5 million (210.5M fully diluted)

Market cap: $284.1 million

Tourmaline Oil (TOU-T)

From world-class operators in mining to an OG of the Canadian oil and gas sector: Tourmaline Oil chairman and CEO Mike Rose. Tourmaline is Canada’s largest natural gas producer and North America’s fifth-largest gas-focused producer, with dominant positions in northeast B.C.’s Montney field and Alberta’s Deep Basin. Rose is a seasoned executive with a track record of making shareholders lots of money.

On Aug. 12 Tourmaline acquired Crew Energy (CR-T) and its Montney gas fields for $1.3 billion and hiked its quarterly dividend, to 35 cents a share (the second increase this year). The market approved, bidding the stock up from $58.28 to a Friday close of $62.95.

The day after the Crew purchase, Rose (left) spent $302,778 to buy another 5,000 Tourmaline shares, paying $60.56 per share. He followed that up on Aug. 16 with a $314,636 purchase of 5,000 shares at $62.93. Rose has spent $4.45 million buying Tourmaline stock so far this year, at prices ranging from $54.82 to $66.43.

Rose's stake in Tourmaline (between personal holdings and his Rose Foundation) is worth about $590 million at the current share price. He is married to Sue Riddell Rose, the CEO of Rubellite Energy (RBY-T) and Perpetual Energy (PMT-T) and the daughter of deceased oilpatch billionaire Clay Riddell, the founder of Paramount Resources (POU-T).

Before founding Tourmaline in 2008, Rose founded, ran and sold two large oil and gas companies:

- Duvernay Oil sold to Royal Dutch Shell for $5.9 billion in 2008;

- Berkley Petroleum sold to Anadarko for $1.5 billion in 2001, eclipsing a hostile bid from Hunt Oil.

Price: $62.95

Shares out: 352.43 million

Market cap: $22.2 billion

Disclosure: I own shares of NGEx Minerals, Mirasol Resources, Aurion Resources, Altius Minerals and Tourmaline Oil. No current business relationship with any company mentioned. This is not financial advice and all investors need to do their own due diligence.